![]() Call us on : +91 9323 295 218 / 022 - 2808 2728

Call us on : +91 9323 295 218 / 022 - 2808 2728

Mutual Fund

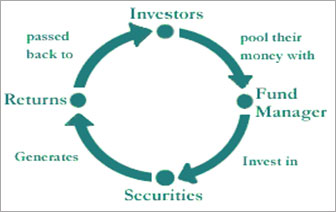

A mutual fund is an entity that pools the money of many investors -- its unit-holders -- to invest in different securities. Investments may be in shares, debt securities, money market securities or a combination of these. Those securities are professionally managed on behalf of the unit-holders, and each investor holds a pro-rata share of the portfolio i.e. entitled to any profits when the securities are sold, but subject to any losses in value as well.

What are the benefits of investing through a mutual fund

Professional Investment Management

Mutual funds hire full-time, high-level investment professionals. Funds can afford to do so as they manage large pools of money. The managers have real-time access to crucial market information and are able to execute trades on the largest and most cost-effective scale.

Diversification

Mutual funds invest in a broad range of securities. This limits investment risk by reducing the effect of a possible decline in the value of any one security. Mutual fund unit-holders can benefit from diversification techniques usually available only to investors wealthy enough to buy significant positions in a wide variety of securities.

Low Cost

A mutual fund let's you participate in a diversified portfolio for as little as Rs.5,000/-, and sometimes less. And with a no-load fund, you pay little or no sales charges to own them.

Liquidity

A mutual fund let's you participate in a diversified portfolio for as little as Rs.5,000/-, and sometimes less. And with a no-load fund, you pay little or no sales charges to own them.

Convenience and Flexibility

You own just one security rather than many, yet enjoy the benefits of a diversified portfolio and a wide range of services. Fund managers decide what securities to trade, collect the interest payments and see that your dividends on portfolio securities are received and your rights exercised. It also uses the services of a high quality custodian and registrar in order to make sure that your convenience remains at the top of our mind.

Transparency

You get regular information on the value of your investment in addition to disclosure on the specific investments made by the mutual fund scheme.

Concept

Mutual Fund Operation Flow Chart

Types of Mutual Funds

Based on your goals and your investment horizon, Mutual Funds give you the option to invest your money across various asset classes like equity, debt and gold. This allows you to diversify your investments and strive to reduce your portfolio risk.

The different types of Mutual Funds are as follows -

Equity Funds / Growth Funds

Funds that invest in equity shares are called equity funds. They carry the principal objective of capital appreciation of the investment over a medium to long-term investment horizon. Equity Funds are high risk funds and their returns are linked to the stock markets. They are best suited for investors who are seeking long term growth. There are different types of equity funds such as Diversified funds, Sector specific funds and Index based funds.

Diversified Funds

These funds provide you the benefit of diversification by investing in companies spread across sectors and market capitalisation. They are generally meant for investors who seek exposure across the market and do not want to be restricted to any particular sector.

Sector Funds

These funds invest primarily in equity shares of companies in a particular business sector or industry. While these funds may give higher returns, they are riskier as compared to diversified funds. Investors need to keep a watch on the performance of those sectors/industries and must exit at an appropriate time.

Index Funds

These funds invest in the same pattern as popular stock market indices like CNX Nifty Index and S&P BSE Sensex. The value of the index fund varies in proportion to the benchmark index. NAV of such schemes rise and fall in accordance with the rise and fall in the index. This would vary as compared with the benchmark owing to a factor known as "tracking error".

Tax Saving Funds

These funds offer tax benefits to investors under the Income Tax Act, 2961. Opportunities provided under this scheme are in the form of tax rebates under section 80 C of the Income Tax Act, 1961. They are best suited for long investors seeking tax rebate and looking for long term growth.

Debt Fund / Fixed Income Funds

These Funds invest predominantly in rated debt / fixed income securities like corporate bonds, debentures, government securities, commercial papers and other money market instruments. They are best suited for the medium to long-term investors who are averse to risk and seeking regular and steady income. They are less risky when compared with equity funds.

Liquid Funds / Money Market Funds

These funds invest in highly liquid money market instruments and provide easy liquidity. The period of investment in these funds could be as short as a day. They are ideal for Corporates, institutional investors and business houses who invest their funds for very short periods.

Gilt Funds

These funds invest in Central and State Government securities and are best suited for the medium to long-term investors who are averse to risk. Government securities have no default risk.

Balanced Funds

These funds invest both in equity shares and debt (fixed income) instruments and strive to provide both growth and regular income. They are ideal for medium- to long-term investors willing to take moderate risks.

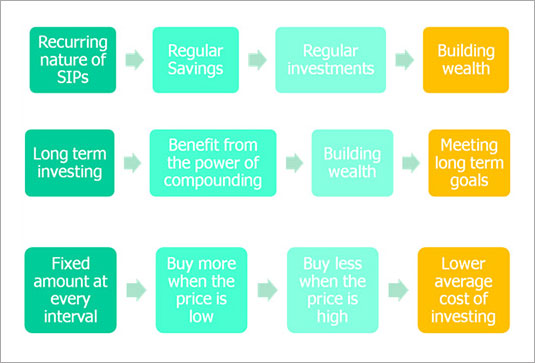

Systematic Investment Plan (SIP)

Presenting Systematic Investment Plan - A Prudent Investment Strategy

What are SIPs?

Systematic Investment Plan (SIP) is an investment technique whereby the investor invests a fixed sum of money at regular intervals, say once a month or once a quarter.

For instance, your SIP may involve

Investing Rs. 5000

- On the 5th of every month

- In a particular scheme of a mutual fund

- For the next five years

Essentially SIPs help avoid 'Decision Paralysis' associated with emotions of fear and greed and takes advantage of ups and downs in the market

Systematic Investment Plan – Illustration

Take Advantage of Rupee Cost Averaging

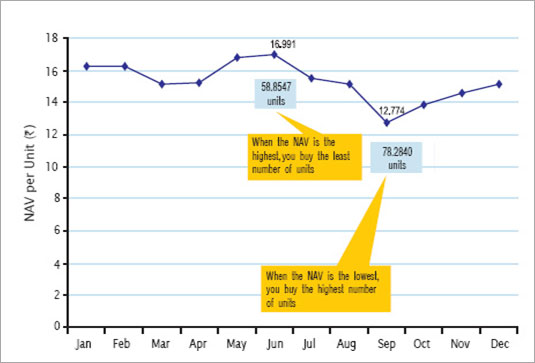

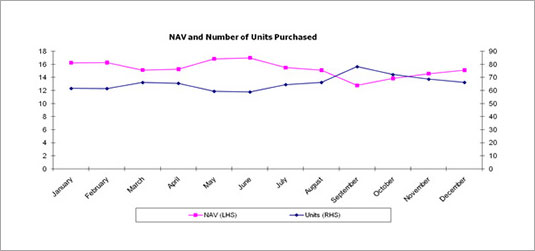

Most investors think that buying stocks at low prices and selling them when prices are high is a favourable strategy. But this is hard to achieve and involves risky variables. A more successful investment strategy is to adopt the method called Rupee Cost Averaging. Under Rupee Cost Averaging, more units are purchased when prices are low and fewer units when prices are high. Imagine investing Rs. 1,000 every month in an equity mutual fund scheme starting in January. The following table illustrates how this investment would have behaved from Jan to Dec.

| Rupee Cost Averaging - An illustration | |||

|---|---|---|---|

| Month | NAV Per Unit* | Amount (Rs.) | Units |

| January | 16.240 | 1,000 | 61.5764 |

| February | 16.266 | 1,000 | 61.4779 |

| March | 15.123 | 1,000 | 66.1244 |

| April | 15.266 | 1,000 | 61.5764 |

| May | 16.845 | 1,000 | 65.5050 |

| June | 16.991 | 1,000 | 59.3648 |

| July | 15.501 | 1,000 | 58.8547 |

| August | 15.114 | 1,000 | 64.5120 |

| September | 12.774 | 1,000 | 66.1638 |

| October | 13.848 | 1,000 | 78.2840 |

| November | 14.566 | 1,000 | 72.2126 |

| December | 15.111 | 1,000 | 68.6530 |

| Total | - | 12,000 | 788.9056 |

*NAV as on the 10th every month. The NAVs are illustrative only.

As seen in the table, by investing through SIP, you end up buying more units when the price is low and fewer units when the price is high. However, over a period of time these market fluctuations are generally averaged and the average cost of your investment is often reduced. In the above table the average cost per unit is approximately Rs. 15.21.

Disclaimer: The illustration above is merely indicative in nature and should not be construed as investment advice. It does not in any manner imply or suggest current or future performance of any Mutual Fund Scheme. Rupee Cost Averaging neither ensures you profits nor protects you from making a loss in declining markets.

SIP automatically ensures that you buy more at lower prices and less at higher prices

Why SIPs?

Systematic Investment Plan – Building wealth

Regular investing for long periods of time deliver healthy returns

An Illustration:

| Monthly Savings - What your savings may generate | ||||

|---|---|---|---|---|

| Savings per month (Rs.) | Total amount invested | Assumed Rate of return (per annum) | ||

| (for 15 years) | (Rs. in Lacs) | 6.00% | 8.00% | 10.00% |

| (Rupees in lacs, 15 years later)* | ||||

| 5,000 | 9.0 | Rs. 14.54 | Rs. 17.30 | Rs. 20.72 |

| 4,000 | 7.2 | Rs. 11.63 | Rs. 13.84 | Rs. 16.58 |

| 3,000 | 5.4 | Rs. 8.72 | Rs. 10.38 | Rs. 12.43 |

| 2,000 | 3.6 | Rs. 5.82 | Rs. 6.92 | Rs. 8.29 |

| 1,000 | 1.8 | Rs. 2.91 | Rs. 3.46 | Rs. 4.14 |

*Monthly instalments, compounded monthly, for a 15-year period.

Disclaimer : The illustration above is merely indicative in nature and should not be construed as investment advice. It does not in any manner imply or suggest current or future performance of any Mutual Fund Scheme. SIP neither ensures profits nor protects you from making a loss in declining markets.

Benefits of SIP

Disciplined investments

(Remember, an investor's worst enemy is not the stock market, but his own emotions)

Reach your financial goals Take advantage of Rupee Cost Averaging, i.e. get more units when prices are low and buy less when prices are high

Grow your investments with compounded benefits. Do all this effortlessly

When you walk a mile, you have actually walked numerous little steps in the right direction…

Similarly, regular savings is a journey and financial goals your destination.

SIPs could be your steps towards meeting your financial goals.